Från marknadsplatser för on-demand-leveranser som hjälper sina kurirer att betala för beställningar till B2B SaaS-företag som ger kunderna tillgång till sina intäkter, måste plattformar ta reda på hur de ska flytta pengar.

Många plattformar följer dock fortfarande manuella processer som saktar ner utbetalningarna.

Beroende på bransch skickar vissa företag papperscheckar, skickar pengar via ACH eller integrerar med olika POS-system.

Att utfärda kort är ett bättre sätt att ge kunderna omedelbar tillgång till medel. Och som en extra fördel har du också möjlighet att skapa ett nytt intäktsflöde. Varje gång en kortinnehavare gör ett köp med ett kort som utfärdats via ditt kortprogram kan du tjäna pengar genom att behålla en del av interchange-avgiften (en kostnad som medföljer varje korttransaktion).

Den här guiden hjälper dig att förstå grunderna för interchange-intäkter. Du får lära dig hur interchange beräknas, hur plattformar kan tjäna pengar på interchange och hur Stripe kan hjälpa till.

Grundläggande om betalningar

Innan du fördjupar dig i interchange är det bra att ha en förståelse på övergripande nivå för hur betalningar fungerar: hur pengar rör sig från en kund till ditt företag och hur banker underlättar dessa betalningar. Att lära sig om dessa grundläggande byggstenar hjälper dig att bättre förstå kostnaderna för detta system och möjligheterna för ditt företag att öka intäkterna.

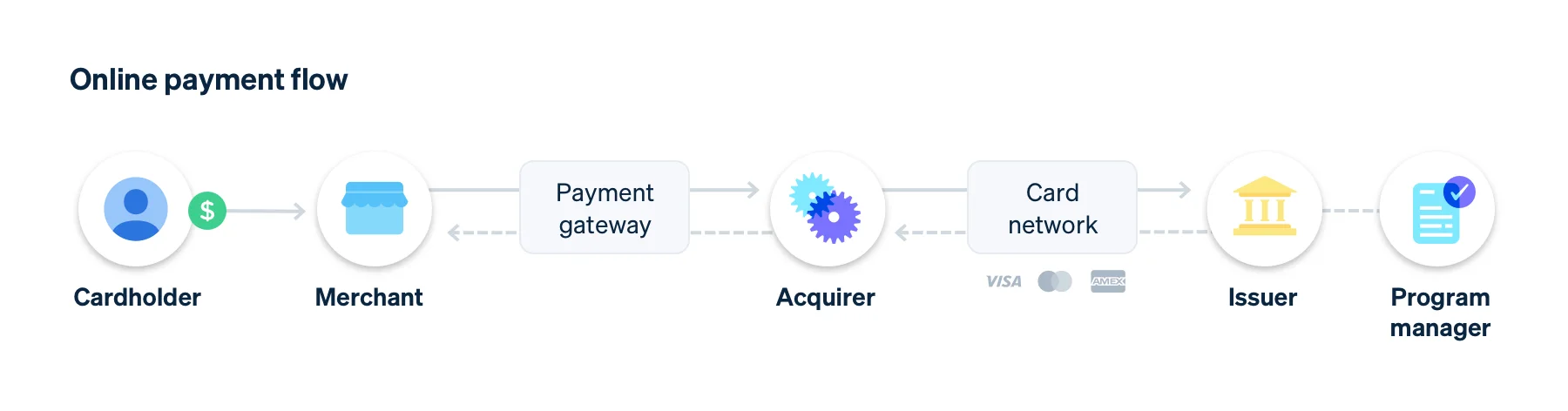

Flera stora aktörer är inblandade i varje transaktion:

- Kortinnehavare: Personen som använder ett kredit- eller bankkort

- Handlare: Den företagsägare som tar emot kortbetalningarna

- Inlösare: Ett finansinstitut som behandlar kortbetalningar på uppdrag av handlare och dirigerar dem genom kortbetalningsnätverk (t.ex. Visa eller Mastercard) till utfärdare. Ibland kan inlösare också samarbeta med en tredje part för att hjälpa till att behandla betalningar.

- Kortbetalningsnätverk: Kortbetalningsnätverk, som Visa och Mastercard, är kopplingen mellan alla dessa parter. De kommunicerar transaktionsinformation, flyttar transaktionsmedel och fastställer de underliggande kostnaderna för korttransaktioner.

- Utfärdare: Banken som tillhandahåller bank- eller betalningsbehandlingstjänster och utfärdar betalkort (t.ex. kreditkort, bankkort, kort eller förbetalda kort) som medlem i kortbetalningsnätverk. De flesta lösningar för utfärdande erbjuder båda dessa tjänster, men vissa företag kan ha två separata relationer (en med betalleverantören och en med en bank).

- Programansvarig: En programansvarig är en icke-bank som samarbetar med utfärdande bank för att göra kortprogram tillgängliga för programchefens kunder. Programansvarig är i första hand ansvarig för allt material och all kommunikation till kortinnehavaren. Programansvarig är föremål för tillsyn av den utfärdande banken och uppfyller vissa efterlevnadsskyldigheter på uppdrag av bankpartnern.

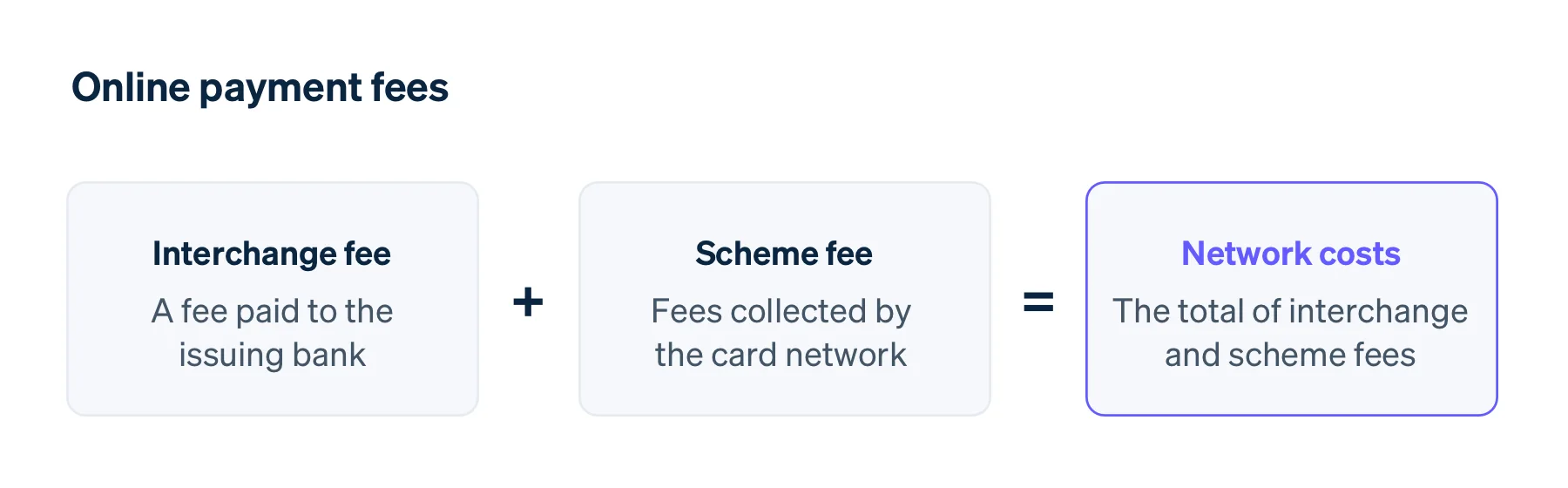

Det finns en mängd olika avgifter som medföljer varje transaktion som behandlas genom detta ekosystem. Visa och Mastercard sätter priserna för:

- De avgifter som tas ut av kortbetalningsnätverket (programavgiften)

- De avgifter som betalas till utfärdaren (interchange-avgiften)

American Express använder en något annorlunda modell eftersom de agerar inlösare, nätverk och utfärdare i ett, och deras nätverkskostnader brukar därmed kallas diskonteringsränta.

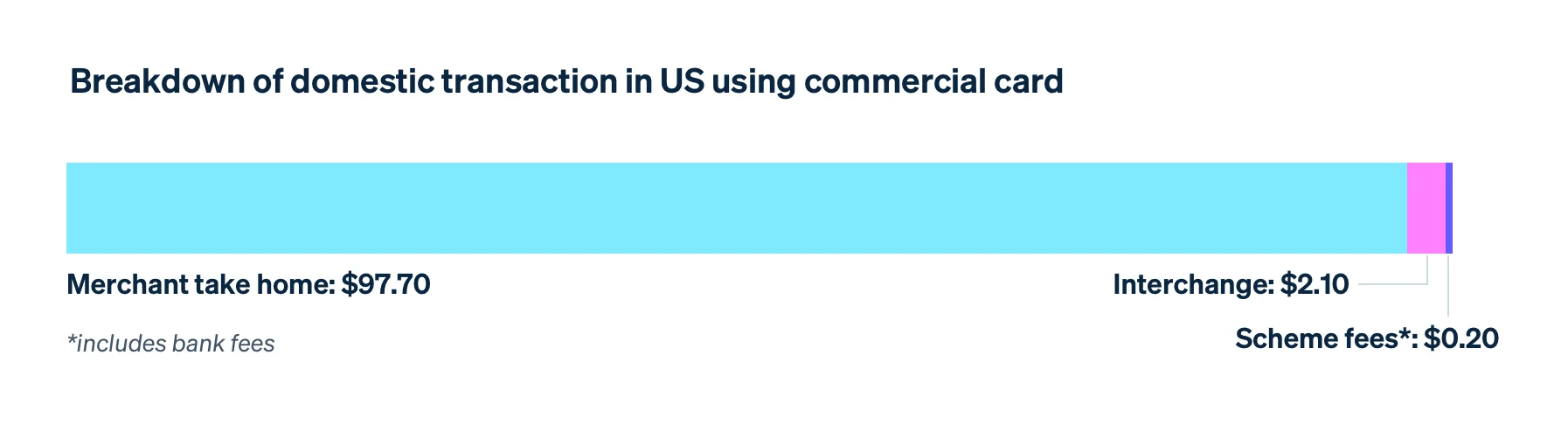

För en inköpstransaktion betalas interchange till utfärdaren eftersom utfärdaren tillhandahåller kort och kundservice och bär kredit- och bedrägeririsken.

Endast banker kan vara huvudmedlemmar i kortbetalningsnätverk och kunna utfärda kort (i USA). För att erbjuda kort till dina kunder kan du arbeta direkt med en utfärdande bank och använda en programvarulösning för att behandla betalningar som används av korten. Detta innebär att du måste hantera bankförhandlingar och partnerskap, efterlevnad av processer som Know Your Customer-skyldigheter och föränderliga regelkrav. Eller så kan du arbeta med en utfärdandelösning som hanterar både utfärdandet och bearbetningen åt dig. En utfärdandelösning erbjuder inbyggda bankrelationer, pålitlig efterlevnad och riskhantering, färdiga arbetsflöden och friktionsfri användar-onboarding.

Med båda uppställningarna skulle du dela en del av interchange-avgiften – antingen med banken eller utfärdandelösningen.

Förmedlingsavgifterna fastställs alltid av nätverket baserat på en uppsättning breda riktlinjer: korttyp (konsument, kommersiellt eller företag), finansieringstyp (kredit, debet eller förbetalt) och om transaktionen är inhemsk eller gränsöverskridande. Interchange-avgifterna regleras också av federal lag.

Interchange-avgifterna för konsumenter är begränsade i Europa på grund av stränga regler. Till följd av detta är förmedlingsavgifterna lägre och plattformar som är baserade i Europa har inte lika stor flexibilitet att påverka sina interchange-intäkter. Kommersiella och företags-interchange-satser är i allmänhet lägre än i USA, även om de inte omfattas av några interchange-tak.

Det finns många undantag från dessa riktlinjer. Till exempel har det genomsnittliga företagskortet högre förmedlingspriser än det genomsnittliga konsumentkortet, men avancerade konsumentkort (som Visa Infinite) resulterar i mer interchange.

Dessa riktlinjer varierar också baserat på ett antal faktorer. Till exempel kan företagskortens avgifter variera baserat hur mycket kortinnehavaren spenderar (ju mer en kund spenderar, desto högre är interchange-räntan).

Ytterligare faktorer som påverkar interchange kan vara:

- Transaktionsstorlek: interchange är ofta en fast procentsats, så den absoluta mängden interchange ökar när kund spenderar mer.

- MCC (Merchant Category Codes): Företag som behandlar kortbetalningar kategoriseras med hjälp av ett MCC. Inköp som görs från företag som tillhör specifika kategorier kan generera mer eller mindre interchange.

- Var handlaren finns: Interchange-nivån ändras om du behandlar en internationell transaktion. Om du till exempel utfärdar ett kort i USA, men kunden gör ett köp med det i Kanada, skulle den transaktionen följa en annan interchange-avgiftsstruktur.

- Type av BIN: BIN (Bank Identification Number) är de sex första siffrorna i ett kreditkortsnummer (2022 kommer BIN att utökas till de åtta första siffrorna). Dessa nummer identifierar kortnätverket, namnet på utfärdande bank, korttyp, kortklass med mera. Beroende på transaktionsinformationen (t.ex. MCC) kan BIN påverka en högre eller lägre interchange-avgift.

Även om du inte direkt kan påverka BIN bör du överväga BIN-support, som möjligheten att blanda och matcha BIN baserat på transaktionen, när du väljer din utfärdandeleverantör.

- Nätverksavtal med handlare: Både Visa och Mastercard erbjuder ofta lägre förmedlingspriser till specifika återförsäljare genom sina partnerprogram: VPP (Visa Partner Program) och MPP (Mastercard Partner Program). VPP- och MPP-räntorna är ofta mycket lägre än de offentliggjorda förmedlingsavgifterna.

- Hur betalningen behandlas: Jämfört med betalningar i fysisk miljö har kortbetalningar en högre sannolikhet att drabbas av bedrägerier. Som ett resultat av detta medför korttransaktioner online en högre interchange-avgift för att kompensera för denna riskökning.

Även om de flesta faktorer beror på själva transaktionen (t.ex. var handlaren befinner sig eller storleken på transaktionen), kan du påverka tre faktorer:

- Typ av kort som används: I allmänhet genererar företagskort, som används för att göra berättigade företagsköp, högre utbyte än konsumentkort.

- Typ av finansiering: I allmänhet har kreditkort, som kräver att utfärdande bank tar större risker, högre interchange-avgifter än bankkort.

- Den utfärdande bankens storlek: För betalningar med bankkort och förbetalda kort har stora banker tillgång till en lägre interchange-ränta än mindre banker, vilket kan påverka hur mycket interchange-intäkter du kan tjäna. Om du till exempel samarbetar med en liten bank för att utfärda kort till dina kunder kommer den del av förmedlingen du får att vara större (eftersom interchange-räntan är högre för de flesta transaktioner).

För att utfärda kort arbetar du antingen direkt med en bank eller arbetar med en utfärdande partner som arbetar med en bank. Du har visst utrymme att välja vilken utfärdare du ska samarbeta med baserat på de banker de arbetar med. Vissa utfärdandepartner kan blanda och matcha kort och banker för att optimera interchange-räntorna för din räkning.

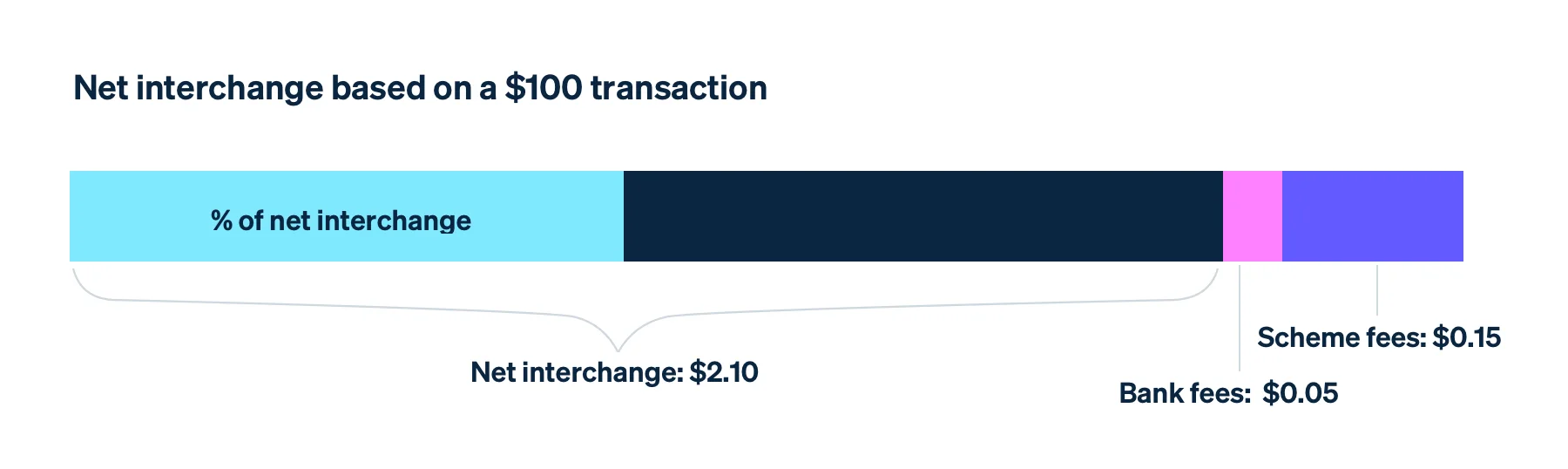

Hur du beräknar dina intäkter från förmedling

Mängden totalt utbyte som åtföljer varje transaktion kallas total interchange (raw interchange). Beroende på ditt partnerskap med en utfärdande partner eller bank och ditt avtal om intäktsdelning behåller du antingen brutto-interchange eller netto-interchange.

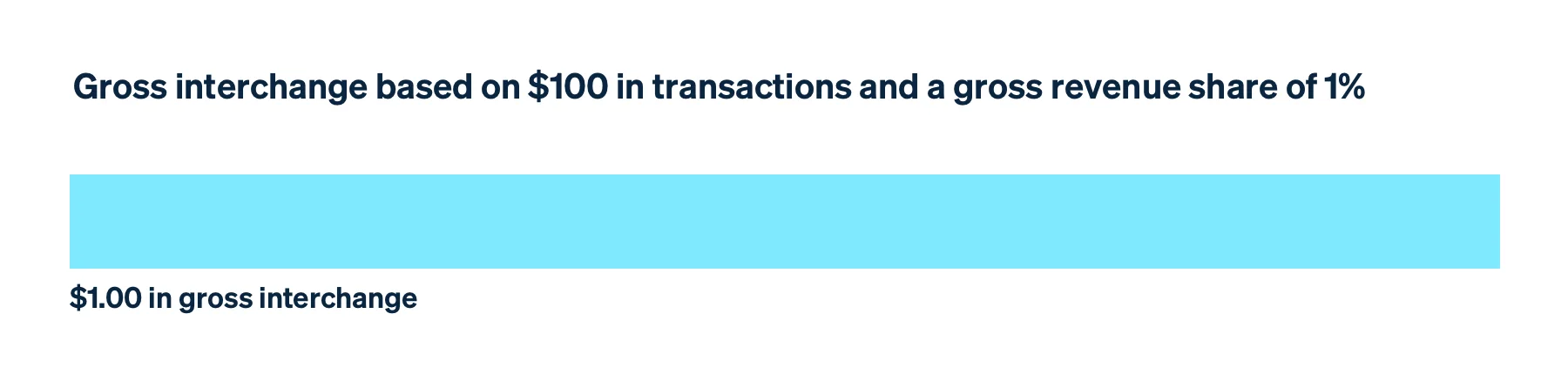

Brutto-interchange

Brutto-interchange är den summa pengar du får baserad på din månatliga transaktionsvolym, oavsett hur mycket interchange som faktiskt genereras. Om du till exempel bearbetade 100 000 USD i transaktioner och du hade en bruttointäktsandel på 1 %, skulle du få 1 000 USD oavsett vad interchange var för dessa köp.

Brutto-interchange är operativt enklare att hantera och ger mer förutsägbarhet än nettoutbyte eftersom du inte behöver oroa dig för avdrag och interchange-räntor på enskilda transaktioner.

Netto-interchange

Netto-interchange är en procentandel av den totala interchange-avgiften efter avdrag för bankavgifter och nätverkskostnader. Procentsatsen varierar beroende på ditt avtal om intäktsdelning.

Detta kan göra det svårare att prognostisera dina intäkter över tid, eftersom du är föremål för varians i den underliggande kostnadsstrukturen och i transaktionsbelopp. Netto-interchange ger dig dock mer insyn i mängden interchange från ditt kort eftersom du kan se hur mycket interchange enskilda transaktioner genererar.

Vad ska man göra med interchange-intäkter?

Oavsett om du får netto-interchange eller brutto-interchange får du ytterligare intäkter. Vissa plattformar väljer att behålla utbytet som en del av sin affärsmodell, vilket skapar ett intäktsflöde som hjälper dem att skala upp.

Andra ger tillbaka en del av eller hela interchange-intäkterna till kortinnehavaren. Ett sätt att göra detta är genom att erbjuda en cashback-belöning, som att ge kunderna 0,25 USD eller 1 % varje gång de använder sitt kort och betala ut dem på månads- eller årsbasis. (Obs: Belöningar är obligatoriska för alla icke-kommersiella kort utöver de lägsta och mest grundläggande priserna.)

Du kan också tänka på mer kreativa sätt att använda dina interchange-intäkter, vilket kan hjälpa dig att differentiera ditt kortprogram och främja mer lojalitet bland dina kunder. I stället för att ge cashback kan du till exempel lägga till medel eller krediter i en plånbok som kan användas på din plattform. Eller så kan du donera en del av eller hela interchange-intäkterna till sociala välgörande ändamål för dina kunders räkning; ett Stripe-företag delar ut kort till sina kunder och donerar en del av interchange-intäkterna tillStripe Climate för att avlägsna koldioxid från miljön.

Så kan Stripe hjälpa till

Plattformar av alla storlekar använder Stripe Issuing för att utfärda kort och skapa nya intäktsströmmar. De använder också Stripes produkter för att inte bara skapa och erbjuda företagskort, utan även för att stödja betalningslösningar, bankkontoersättningar och företagsfinansiering.

Stripe erbjuder en mängd olika produkter som gör att du enkelt kan integrera dessa finansiella tjänster direkt i din plattform:

Stripe Connect

Stripe Connect hjälper dig att genomföra onboarding och hantera dina användare och göra det möjligt för dem att ta emot betalningar för sin verksamhet.

- Genomföra onboarding av användare: Registrera dina användare, slutför KYC och verifiera deras identitet för att stödja dina efterlevnadskrav.

- ta emot betalningar: Ta emot och underlätta betalningar på uppdrag av din programvaruplattforms användare eller deltagare på din marknadsplats.

- Hantera och tjäna pengar på betalningar: Hantera användare på din plattform och tjäna pengar via intäktsandel eller påslag på betalningar och tilläggstjänster.

Stripe Capital

Stripe Capital ger dig ett sätt att erbjuda kunder snabb och flexibel finansiering om de behöver komplettera sin betalningsvolym. Det är ett end-to-end-utlånings-API som hjälper kunder på din plattform att växa samtidigt som de tjänar en intäktsandel på alla lån som förlängs, utan ekonomiskt ansvar för kreditförluster.

Stripe Treasury

Stripe Treasury låter sedan dina användare lagra pengarna de tjänar genom betalningar eller som de får genom finansiering. Med vårt inbyggda API för finansiella lösningar kan du bädda in finanskonton direkt i din plattform så att användarna kan betala räkningar och hantera sitt kassaflöde.

- Snabbare medel: När medel skickas till Stripe kan vi flytta pengar snabbare än det traditionella banksystemet. När medlen finns i ett system är det helt enkelt en huvudbokshändelse.

- Lagra medel för dina kunder: Gör det möjligt för dina kunder att behålla medel på din plattform och bli den främsta destinationen för dem att lagra, hantera och flytta pengar.

Stripe Issuing

Stripe Issuing kan låta dina användare spendera sina medel via kort. Stripe tillhandahåller den infrastruktur som du behöver för att bygga och hantera kort för din plattform.

- Utfärda kort omedelbart: Skapa virtuella kort direkt eller ge ut fysiska kort så snabbt som på två arbetsdagar.

- Kontrollera programmatiskt: Kontrollera utgifter och hjälp till att förhindra bedrägeri genom att sätta utgiftsgränser, blockera typer av företag eller skapa avancerade kombinationer av regler.

- Monetarisera: Användare som når en viss volymtröskel får en procentandel av interchange-avgiften från alla kortköp. Stripe använder brutto-interchange, vilket hjälper till att effektivisera verksamheten och ger förutsägbarhet i kassaflödet.

För mer information om Stripe Issuing,läs våra dokumentation. För att skapa dina egna virtuella och fysiska kort direkt,registrera ett konto.